Tail wags the dog, or...? July sentiment manipulation + Intraday post (27/June)

Weekly post

Revised-weekly post on dynamics and Fed

Looming Fed pivot

Tail wags the dog, or dog wags the tail, or these are both the same as Jung would have say?

After you done read the above linked posts, I want to emphatize that we are still in a net short vanna regime, but way flatter than before. The tenors are different. This week is characterized by vol selling as predicted (I only underestimated the effect of geo risk unwound, and vol actually made lower lows, after spot broke out of the range). Vomma supply remains on the monthly tenor, but on the shorter-tenors the bet is a VIX vega up, potentially expecting an SPX squeeze up into July 4, and that would push the dealer positions through the center of the long fly in VIX, and flatten further the SPX short vanna flow, that is still being materialized.

Overall vomma selling seems remain with us into July. And vol can slowly start to catch a bid that would start to have a suppressive effect on the index, if VIX holds firmly below 16.5, but wouldn’t really fall, only ranging, bcs the short speed profiles below act like a stunt mats towards any downside move.

The key point is sentiment. That is artificially held up on dovish hopes.

Both Fed, Bessent and algos made market taking bad news as good news.

To fully understand this, you have to remember what I’m always telling you: when you listen to the news, always ask the question “why now, what do they want to sell me?”, bcs on the Street sentiment is also literally a product. Always watch the timing first, not the content. Content only matters in the context. Read about the terms of ‘reflexive control’.

And the other thing is, that the whole system is just numbers going up and down. There are dynamic correlations (positive/negative) between different metrics etc. that algos are constantly monitoring (especially the trend of the changes!!) and so they trade based on it. So, this way, the tail starts to wag the dog, while the dog also wags the tail. A reflexive, self-fulfilling system.

And a strong hand from the outside, like Bessent, can add other trends, values to this machine, that shifts the algo sentiment a bit.

(I keep talking about the ‘hidden QE’ since April 13th, since SPX was at 5363.35).

The reason for this sentiment manipulation is that they know that tariff effects ad other supply chain problems that I painted for you in April, are about to come, and will slowdown growth. Not necessary recession, 40-45% I assume only, but a strong, persistent stagflation.

But Trump is about to pump growth for any price, as much as he can until reality starts to loom in. This is expected into July FOMC, and August (something that I first wrote about in April 24th). In April, I spent a lot of time to explain these processes for you very detailed. Check them back.

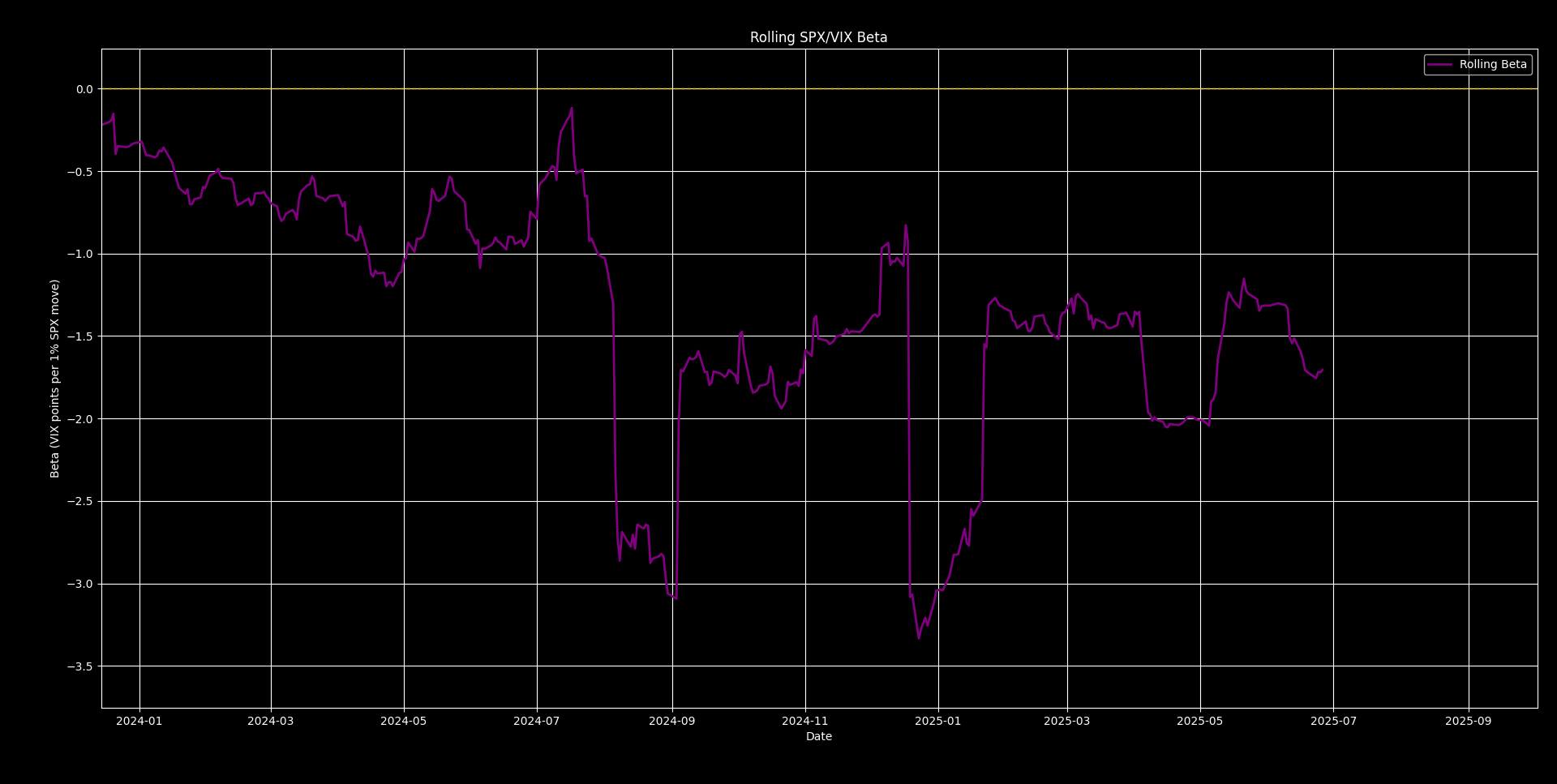

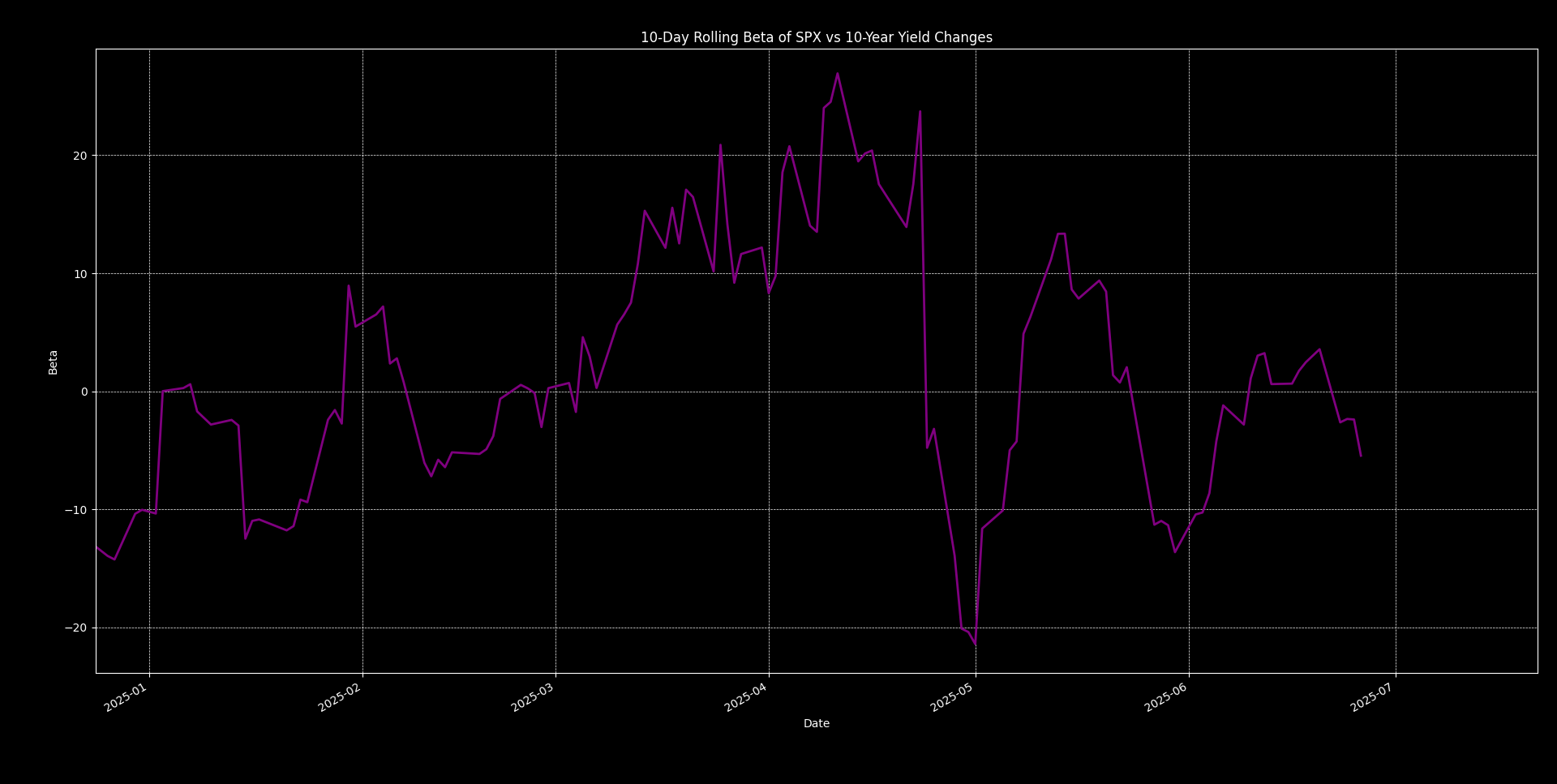

So, sentiment is prepared to take recessionary datas positively. Pricing in a dovish tilt into July FOMC. Then I expect SPX/yields beta going back to positive, and a selling flow, on a ‘no-cut’ scenario. Odds are significantly high on this. (no vol squeeze, but a coordinated selling flow).

Why?

Because big money is on the sideline. Money-market funds now hold $7 trillion in assets, the most ever. With yields so attractive, institutional cash (MMFs, pension funds) has frozen in these short‐dated instruments rather than flowing into stocks. That creates an illiquid market for equities, with heavy supply on the sidelines. If the Fed would actually cut rates, t-bill yields would fall, making money funds less attractive, triggering an outflow from MMFs into equitites. If no-cuts happen, dollar would strenghten and we would see a slow, coordinated sell. This is a pivotal event if we are in a bear market or not. Remember the stagflation rally of the 70s...

If GDP, PMI, payroll etc are weak enough, the market bet can be fullfilled.

Until we can expect a net rangebounding basically accumulating zomma and vomma risk into August, while and vol spike will be managed through vol of vol supply, and if regime can’t shift, bcs July 8-9 pushes SPX back after a potential squeeze up out of short vanna regime (as I expect), then vol grind up can start, slowly (in a stairstep manner).

Let’s jump into the daily outlook…