Fed pivot is looming? Tariff risk, Sentiment + Intraday post (26/June)

Yesterday I revised my weekly post after the market broke out of the weekly range and unwound a lot of geo risk positions from Monday to Tuesday.

It is half-free, and educational on distributions. Take your time on it…

Let me show you something…

FFF6 is the June 2025 Fed-funds futures contract. Its implied rate has fallen to 0.6350%

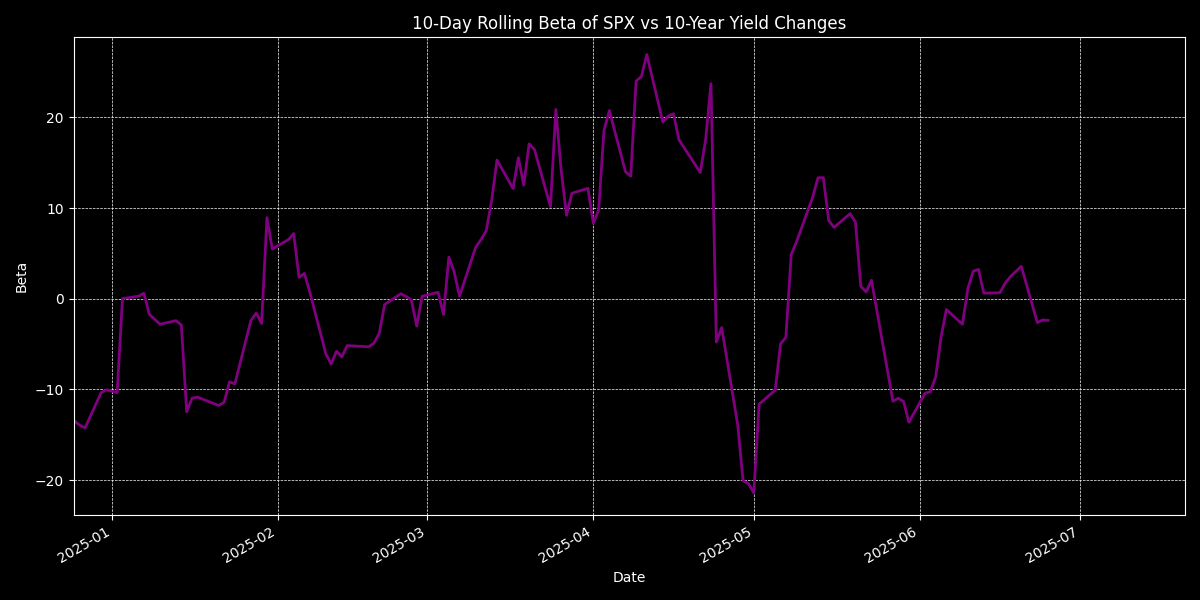

The 5-yr vs 30-yr Treasury spread keeps widening, a bear-steepening sign as the belly price moves on front-end rate-cut bets even while long-end yields stay elevated on fiscal concerns.

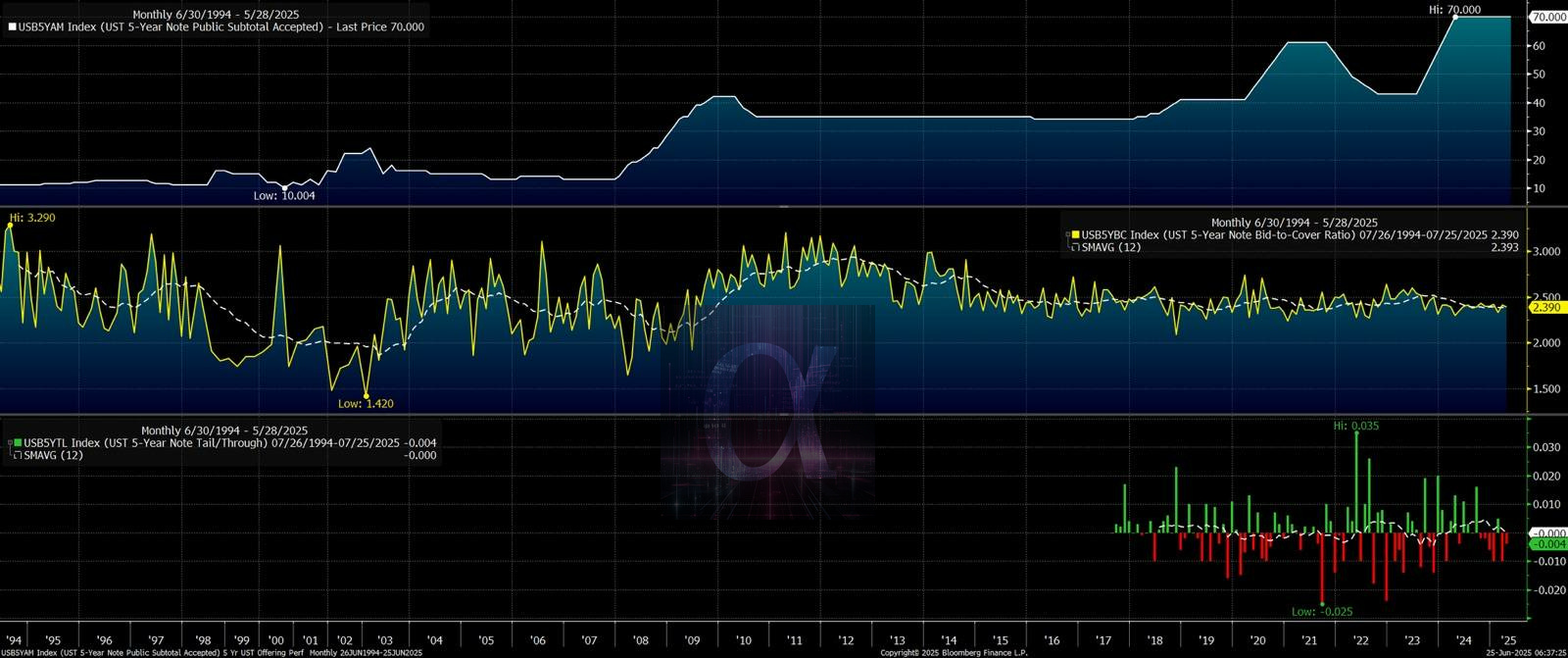

This tells us demand held, but only at current yields—so any “dovish shock” (e.g. weak NFP → Fed cut) would likely drive 5-year yields sharply lower.

Also note, that the Nasdaq/Russell ratio (not shown here) sitting at multi-year highs underscores that mega-caps are front-running any dovish pivot, even as broader cyclicals lag. Fed driven deltas. In dovish regimes, frontrunning pivots, mega-cap tech often outperforms, lifting this ratio, whereas in reflationary or risk-on phases, small caps can lead.

Market prices a Fed pivot on a bad NFP print. As I mentioned in the weekly post and earlier, sentiment is artificially shifted towards “bad news are good news”. But with hgiher lows, as recession fears are looming into August-Sept window.

With no August FOMC meeting, the Fed can use July data to gauge tariff-driven inflation before acting.

I expect a potential stagflationary slowdown into August, cutting their 2025 GDP at ~1.3% and recession fears coming back, driven mostly by tariff-induced growth drag and persistent inflation.

Bessent’s buybacks help temporaly mitigate a yield shock, supporting equities if tariffs spark a rise in long-end yields. If August inflation prints show only a temporary tariff bump, markets may still price in Fed cuts by Q4, bolstering risk assets.

My thoughts on these…

To me this market seems like aims to be supported into July 4, and tries to swallow any impact of the July 8-9 reciprocal-tariff deadline—when the 90-day pause on Trump’s “Liberation Day” duties expires.

The NQ/RTY ratio spikes not just on fundamentals but also because rapid, vol-sensitive flows concentrate in mega-caps (lower gamma cost); dealer hedges and ETF rebalances then narrow breadth by reinforcing the winners. Every dip in tech (or bounce in vol) triggers a wave of vol-control and gamma-hedge buying—lifting the ratio further, even if small-caps or cyclicals lack fundamental momentum.

But once July 8’s tariff cliff and August catalysts arrive, volatility control funds will sell into rising vol, CTAs will squeeze out of steepeners, and buybacks can’t absorb a broad sell-off—so both yields and equities may snap back sharply. However these sentiment-driven interventions mitigate the raw auction, curve and Fed-futures signals in the near term. So, no vol squeeze event… Vol of vol supply, you know…

I will signal short, when I see that.

Let’s jump in to the daily setup…