Weekly post (12-16/May)

The pivotal week

I already shared my current main bias for this week. It didn’t changed, but in this post I will share the levels and the momentum that I’m looking for.

Credit spreads are still very tight by historical standards but have crept wider since mid-2024.

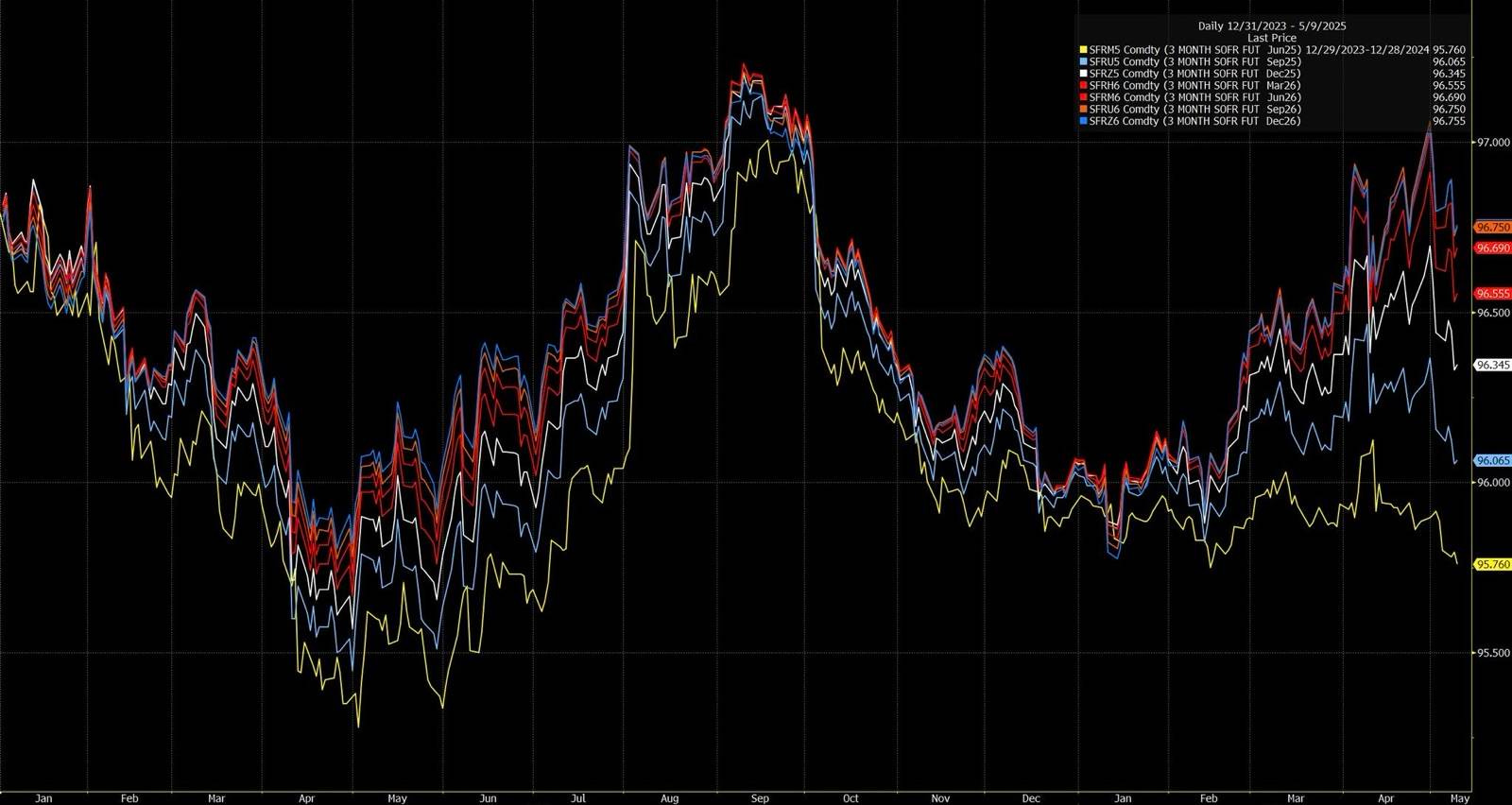

The Fed’s balance-sheet runoff has driven reserve balances down to about $3.2 trillion and reverse-repo usage to roughly $155 billion, though weekly flows remain erratic. SOFR futures trade around 95.75 for June ’25 and rise to about 96.46 for December ’25—implying a peak SOFR near 4.25 percent and cuts back toward 3.5–3.6 percent by year-end.

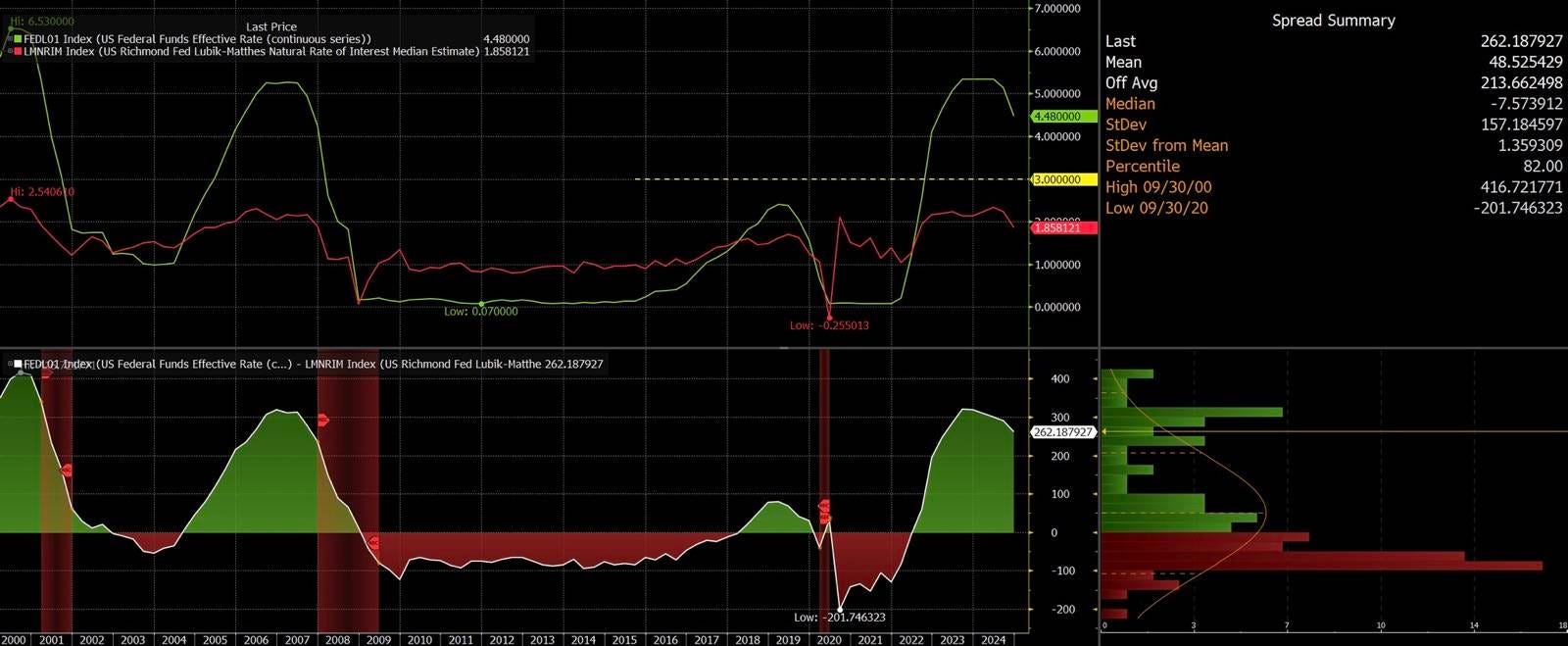

The effective fed funds rate sits at 4.33 percent, about 247 basis points above the Richmond Fed’s 1.86 percent neutral estimate, signaling a restrictive stance.

And on May 11, China called the Geneva talks “candid, in-depth and constructive” and said a joint statement with “good news” will follow soon. The talks appear to have produced a formal accord on narrowing the bilateral deficit and de-escalating tariffs, with details imminent. Very important event, and the timing is not a coincidence…

SOFR futures are pricing in an imminent peak and a series of rate cuts stretching into 2026. Policy stance remains explicitly restrictive (Fed funds > neutral by ~2.6 pp), even as markets lean toward easing ahead.

Fed is in tightening/normalization mode but with markets already looking for the pivot—and credit conditions beginning to reflect a bit more stress. Longer-run forecasts (3.5–4 %) imply the Fed will likely keep policy restrictive through 2025 before easing. April CPI is expected to show a modest uptick but remain well below mid-2022 highs.