ANNOUNCEMENT

I won’t work between July 24 and Aug 1, I will create one chat room for that period, and I will be here on FOMC day, but there will be no intraday posts in that period.

In Friday post, I wrote macro:

The momentum is bullish for now, profits getting taken, volume is low, and liquidity is unstable. All what you see is mechanical flows and short-term speculative tradings and short squeezes. And I’m pretty sure that this trend will hold until FOMC, that is my main risk target since May. This is why I keep emphatizing since June 24, that don’t rush to short this market yet.

But market needs Powell to comfirm it. If no Fed cut, no yield relief = no cash out of MMFs, meaning no liquidity boost for equities. Market support from short‑term liquidity evaporates, causing a significant unwind of the current, liquidity‑driven rally. Simply because the liquidity lifeline stays locked into MMFs and T‑bills. Lower front‑end yields have been a key catalyst for equity rallies. And this is what the Fed can control, the long-end is owned by the investors. So, as Treasury issuance outstrips MMF absorption capacity, yields will spike, liquidity will decline, and this fake growth rally will unravel.

The thing is that since the 2000s the M2 went from 4.7 trln to 21.94 trln USD, while total market value from 13.45 trln to 62.2 trln USD. So it means that excess liquidity has been the primary driver of soaring stock valuations, rather than proportional growth in real economic output.I strongly think that when equities start to fall, BTC will go with them as well, the way it did in April:

Money goes from risk assets to safe-havens, then allocate a portion of it into digital assets and some back to legacy markets. And so on. Deposits must be washed slowly out and market needs new home.

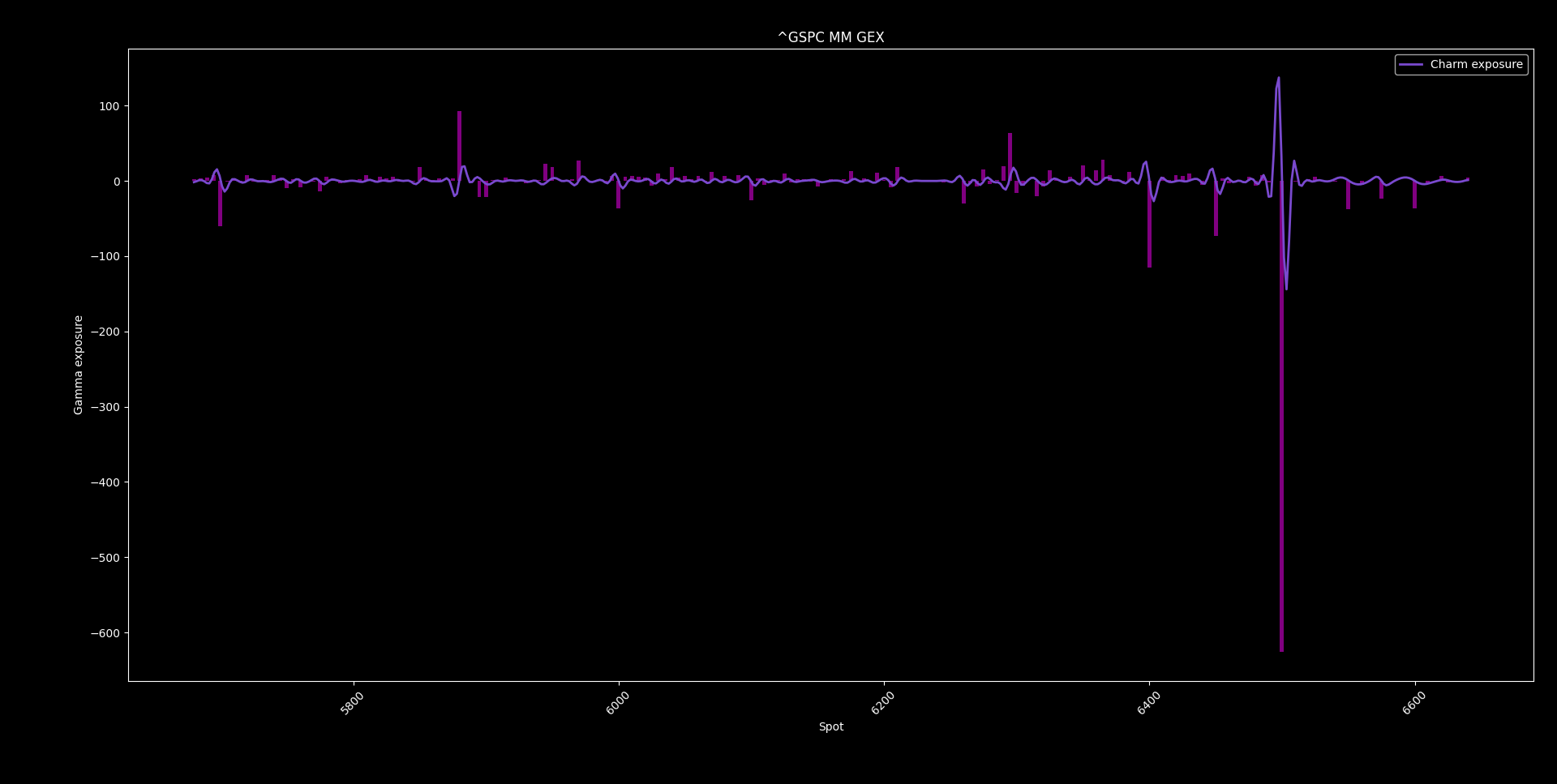

Monthly positioning

This is how month end looks like now, taking into account the vol effect of Aug - Sept - Dec tenors: